Key Takeaways

- The Net Price Calculator is the most accurate free tool for estimating your actual out-of-pocket college cost before you apply — every college receiving federal aid is required to have one on their website.

- Net price (what you actually pay) can be dramatically different from sticker price (published tuition) — at many private schools, the average student pays 40–60% less than the advertised cost.

- NPC results vary significantly by family income, assets, and school — running the calculator at each school you’re seriously considering is essential for making an informed application list.

- NPC estimates are not binding offers — actual financial aid awards may differ based on the formal application, verification, and the school’s available aid budget — but they’re far more useful than sticker price for planning purposes.

Table of Contents

What Is a Net Price Calculator?

I talk to families every week who are making college decisions based on published tuition numbers — and almost all of them are doing it wrong. The sticker price on a college’s website is not what most students pay. It’s the starting point before financial aid, grants, and scholarships are applied. The Net Price Calculator (NPC) is the tool that shows you what you’d actually pay — and the difference can be staggering.

Every college and university that receives federal financial aid is legally required to have a Net Price Calculator on their website under the Higher Education Opportunity Act. The tool takes your family’s financial information and estimates your grant aid eligibility, subtracting it from total cost of attendance to show your estimated net price. It’s not perfect — we’ll get to limitations — but it’s the closest thing to a real cost estimate you can get before applying. According to the Department of Education’s College Affordability and Transparency Center, the gap between sticker price and actual net price is significant at most institutions.

⚡ Pro Tip

Run the Net Price Calculator at every school on your list before finalizing your applications — not after you’ve been admitted. The results can dramatically reshape which schools are actually affordable for your family. A school with $65,000 sticker tuition might net out at $22,000 for your income bracket, while a $40,000 sticker school offers almost no aid and nets at $36,000. The NPC reverses what looks “affordable” at first glance.

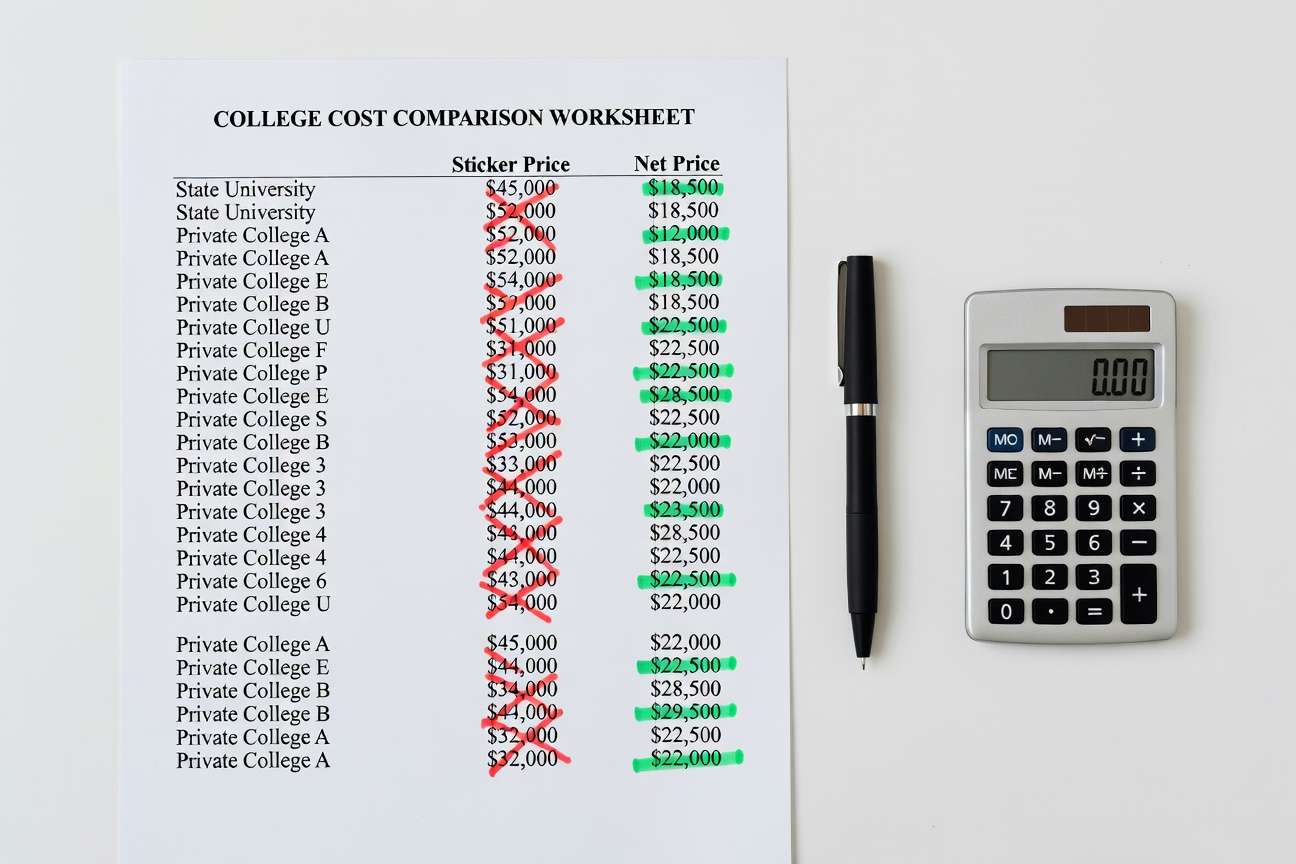

Sticker Price vs. Net Price: The Real Difference

Let’s make this concrete. A highly selective private university might publish a total cost of attendance — tuition, fees, room, board, books, personal expenses — of $85,000 per year. That number is real and technically accurate. But for a family earning $65,000, that same school might offer $63,000 in grant aid, making the actual net price $22,000. Meanwhile, a state university with a $28,000 in-state sticker price might offer $5,000 in aid, netting at $23,000.

The schools cost nearly the same — but the family that assumed “expensive private school, definitely can’t afford it” never even visited the NPC and ruled it out. This happens constantly, and it costs students access to schools that are genuinely affordable for them. The relationship between sticker price and actual cost is loose and non-linear, especially for middle- and lower-income families at well-endowed private institutions. Sticker price is useful for roughly understanding a school’s scale; net price is what determines whether you can afford it.

How to Use a Net Price Calculator

Finding a school’s NPC is straightforward: go to the school’s financial aid website and search for “Net Price Calculator” or “Estimate Your Cost.” You can also access a directory of NPCs through the Department of Education’s NPC directory. Most schools use one of a few standard NPC platforms — the College Board’s tool, or a school-specific version. Some elite schools have built their own sophisticated calculators that come very close to the actual aid formula.

Work through the calculator completely and honestly. Don’t round numbers in your favor or leave fields blank — the accuracy of your result depends entirely on the accuracy of your inputs. Run the same calculator twice if you want to check your work. And run it for every school you’re genuinely considering — the results vary enough across institutions that you need school-specific estimates, not a general average.

What Information You’ll Need

Most Net Price Calculators ask for a consistent set of information drawn from your family’s tax returns and financial records. Have these ready before you start: parent(s) adjusted gross income from the most recent tax return, parent(s) total assets (savings, investments, home equity — though some NPCs don’t ask about home equity), number of people in the household, number of college students in the household simultaneously, and sometimes the student’s own income and assets if applicable.

Some NPCs also factor in academic merit — GPA, test scores — for merit aid estimates. Have those numbers available. The whole process takes about 10–15 minutes per school once you have your financial documents in front of you. For the most accurate results, use the same tax year’s numbers across all schools so you’re comparing apples to apples. For context on the full financial aid process this calculator fits into, our complete financial aid playbook covers FAFSA through award letters.

| School Type | Avg. Sticker Price | Avg. Net Price | Typical Discount |

|---|---|---|---|

| Elite Private (Ivy+) | $82,000–$90,000 | $8,000–$22,000 | 75–90% |

| Private Liberal Arts | $58,000–$72,000 | $18,000–$32,000 | 50–70% |

| Public Flagship (In-State) | $26,000–$35,000 | $14,000–$22,000 | 20–40% |

| Public Flagship (Out-of-State) | $50,000–$65,000 | $38,000–$55,000 | 5–20% |

| Community College | $8,000–$14,000 | $2,000–$8,000 | 40–75% |

| Key Insight: Elite private schools often cost LESS than out-of-state public flagships for middle-income families. Always run the NPC — never assume based on sticker price. | |||

Interpreting Your Results

When your NPC results appear, you’ll typically see: total cost of attendance, estimated grant aid, estimated net price, and sometimes a breakdown that includes loans and work-study. Here’s the critical read: focus on grants and scholarships only. That’s the actual discount from cost of attendance. Loans are debt you’ll repay — they don’t reduce what you pay, they just defer it. Work-study is earned wages — also not a discount.

Your true estimated net price = Cost of Attendance minus grants and scholarships. Everything else in the “aid” column is either borrowed or earned. If the NPC gives you one combined “aid” number, try to find the breakdown before drawing conclusions. Many NPCs do provide the grant-only figure — look for “gift aid,” “grants and scholarships,” or “free money” specifically. That number subtracted from COA is your honest estimate of annual cost.

NPC Limitations to Understand

Net Price Calculators are useful but imperfect, and the limitations matter. They’re estimates — not offers. The actual aid award you receive after submitting a full financial aid application may differ from the NPC result due to verification of income, updated financial information, or the school’s available budget in a given year. NPCs are typically updated annually but may lag by a year in reflecting current aid levels.

They also generally don’t capture all merit aid accurately. If a school awards significant merit scholarships based on GPA and test scores, the NPC may underestimate your aid if it doesn’t have a robust merit component. And some NPCs are simply less accurate than others — the most carefully built ones (often at schools with large endowments and need-blind admissions) are quite close to actual awards; others are much rougher approximations. Treat results as directional estimates with a margin of error of roughly ±$3,000–$5,000 annually, not as guaranteed figures.

⚡ Pro Tip

When comparing NPC results across schools, make sure you’re comparing the same components. Some NPC outputs include loans and work-study in the “aid” figure, making net cost look lower than it really is. Always find the “grants and scholarships only” line and subtract only that from the total cost of attendance. Loans aren’t aid — they’re debt you’ll repay. Work-study isn’t a discount — it’s wages you’ll earn. True net price = COA minus grants and scholarships only.

Building Your College List Around Real Costs

The most financially rational approach to building a college list starts with NPC results, not rankings or reputation. Run every school you’re considering through its NPC. Create a simple spreadsheet: school name, total COA, estimated grants, estimated net price, and your affordability threshold. Sort by net price. Let the results inform which schools are reaches, matches, and safeties from a financial standpoint — not just an academic one.

A financial safety school is one where you know the NPC result is affordable regardless of how much aid you receive — because even the worst-case scenario is manageable. This might be your state’s flagship, a community college with transfer agreements, or a school known for generous aid to your income bracket. Build at least one true financial safety into every list. For full context on decoding the award letters you’ll receive after applying, our guide on understanding your financial aid package walks through every line item.

References

- U.S. Department of Education (2026). “Net Price Calculator.” collegecost.ed.gov

- Federal Student Aid (2026). “How Aid Is Calculated.” studentaid.gov

- Consumer Financial Protection Bureau (2025). “Paying for College.” consumerfinance.gov

- Investopedia (2025). “Net Price Calculator.” investopedia.com