Quick Answer

Your credit utilization ratio — the percentage of available revolving credit you’re using — is the second-largest factor in your FICO score, accounting for 30% of the total. Keeping it below 30%, and ideally under 10%, can meaningfully raise your score. As of July 2025, experts consistently identify high utilization as one of the fastest-fixable score killers.

Your credit utilization ratio is calculated by dividing your total revolving credit balances by your total revolving credit limits, then multiplying by 100. It carries more weight than most borrowers realize — according to myFICO’s official credit education resources, this single factor makes up 30% of your FICO score, second only to payment history at 35%.

Understanding how utilization works — and how to control it — can be the difference between a good score and a great one. This guide breaks down exactly how the ratio is calculated, what thresholds matter, and which strategies move the needle fastest.

Key Takeaways

- 30% of your FICO score is determined by amounts owed, with credit utilization ratio being the dominant component of that category (myFICO).

- Consumers with FICO scores above 800 carry an average utilization rate of just 7%, according to Experian’s credit utilization research.

- A utilization rate above 30% is widely flagged as a risk signal by lenders and all three major credit bureaus: Equifax, Experian, and TransUnion (Consumer Financial Protection Bureau).

- Paying down a balance to reduce utilization from 90% to 30% can raise a FICO score by as much as 100 points in some cases, per Experian’s scoring analysis.

- VantageScore 4.0, used by many lenders alongside FICO, also treats utilization as a “highly influential” factor in its scoring model (VantageScore).

In This Guide

- What Exactly Is a Credit Utilization Ratio?

- How Does Credit Utilization Ratio Affect Your Credit Score?

- What Is the Ideal Credit Utilization Ratio?

- Does Per-Card Utilization Matter as Much as Overall Utilization?

- How Can You Lower Your Credit Utilization Ratio Quickly?

- What Common Mistakes Destroy Your Credit Utilization Ratio?

- Frequently Asked Questions

What Exactly Is a Credit Utilization Ratio?

Your credit utilization ratio is the percentage of your total available revolving credit that you are currently using. It applies to credit cards and lines of credit — not installment loans like mortgages or auto loans.

How to Calculate It

The formula is straightforward: divide your total revolving balance by your total revolving credit limit, then multiply by 100. For example, if you carry a $2,000 balance across cards with a combined limit of $10,000, your utilization is 20%.

Credit bureaus calculate this ratio both overall (across all cards) and per individual account. Both figures influence your score. The Consumer Financial Protection Bureau (CFPB) recommends reviewing your credit report regularly to ensure reported balances are accurate before your ratio is calculated.

Credit card issuers typically report your balance to the credit bureaus once per month — usually on your statement closing date, not your due date. This means your reported utilization may be high even if you pay in full every month.

What Counts as Revolving Credit

Revolving accounts include credit cards, retail store cards, and personal lines of credit. Fixed installment debt — such as student loans, auto loans, and mortgages — is tracked separately and does not factor into utilization calculations. If you are managing student debt alongside credit card balances, the amortization dynamics of installment loans work very differently from revolving credit.

How Does Credit Utilization Ratio Affect Your Credit Score?

Utilization directly impacts your score because it signals to lenders how dependent you are on borrowed money. High balances relative to limits suggest financial stress — even if you pay on time.

Its Role in the FICO Scoring Model

FICO, the dominant credit scoring model used by most U.S. lenders, breaks its score into five weighted categories. The “amounts owed” category — where utilization lives — accounts for 30% of your score, as detailed by myFICO’s scoring breakdown. Only payment history (35%) carries more weight.

Within the amounts-owed category, the credit utilization ratio is the single most influential sub-factor. Other elements — such as the number of accounts with balances and the amount owed on installment loans — matter, but utilization is the primary lever you can adjust quickly.

“Reducing your credit card balances is one of the most effective ways to improve your FICO score in a relatively short period of time. Unlike payment history, which takes years to build, utilization can change from month to month.”

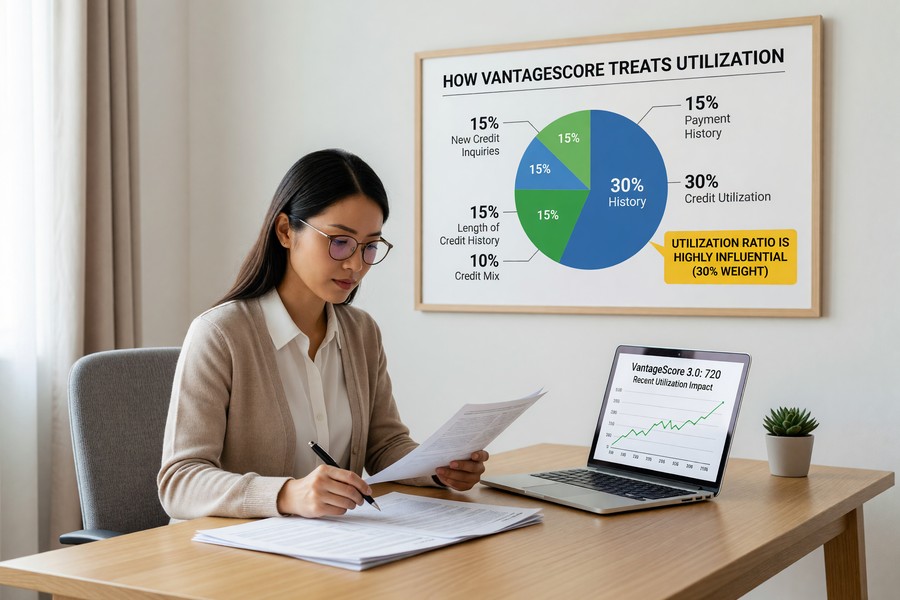

How VantageScore Treats Utilization

VantageScore, the competing model jointly developed by Equifax, Experian, and TransUnion, also classifies credit utilization as “highly influential.” According to VantageScore’s consumer education page, it is one of the top two factors in its model — meaning the impact holds regardless of which scoring system a lender uses.

What Is the Ideal Credit Utilization Ratio?

The most credit-score-friendly utilization rate is as low as possible — with under 10% being the sweet spot for top-tier scores, and under 30% being the broadly accepted minimum target.

| Utilization Range | Score Impact | Lender Perception |

|---|---|---|

| 1%–9% | Maximum positive effect | Excellent — minimal credit reliance |

| 10%–29% | Good — minor negative signal | Acceptable for most lenders |

| 30%–49% | Moderate negative impact | Elevated risk flag |

| 50%–74% | Significant negative impact | High-risk indicator |

| 75%–100% | Severe score damage | Near-maxed — serious concern |

Why Zero Percent Is Not Ideal

Carrying a 0% utilization — meaning no balance at all — can actually be slightly less favorable than carrying a very small balance. Experian’s utilization guidance notes that some activity on revolving accounts signals to scoring models that you are actively managing credit. A balance of 1%–9% demonstrates responsible use without risk flags.

Americans with FICO scores of 800 or above maintain an average credit utilization of just 7%, according to Experian’s State of Credit report — compared to a national average closer to 28%.

Does Per-Card Utilization Matter as Much as Overall Utilization?

Yes — scoring models evaluate both your overall utilization across all accounts and the utilization on each individual card. A single maxed-out card can hurt your score even if your aggregate utilization is low.

The Per-Card Problem

If you have three credit cards and one is at 90% utilization, that individual card’s ratio registers as a risk signal — regardless of what the other two cards show. FICO scoring algorithms penalize high utilization at the account level, not just the portfolio level. This is why spreading balances across multiple cards is generally better than concentrating debt on one.

Managing debt across multiple accounts also connects to broader financial habits. If you are working through aggressive debt payoff strategies, the same avalanche and snowball principles that work for student loans can be applied to revolving credit balances.

Authorized User Accounts

If you are listed as an authorized user on someone else’s credit card, that card’s utilization typically appears on your credit report as well. A high-utilization account belonging to the primary cardholder can drag down your score — even though you are not responsible for the debt. Review your credit reports at AnnualCreditReport.com to identify any such accounts.

Closing an old credit card immediately reduces your total available credit, which can spike your overall utilization ratio overnight — even if you carry no balance on the card you closed. This is one of the most common unintentional credit score mistakes.

How Can You Lower Your Credit Utilization Ratio Quickly?

The fastest ways to reduce your credit utilization ratio are paying down existing balances, requesting a credit limit increase, and timing your payments strategically before the statement closing date.

Pay Before the Statement Closes

Because issuers report balances on your statement closing date, paying down your card before that date — not just before the due date — means a lower balance gets reported to the bureaus. This single timing shift can improve your reported utilization by 10–20 percentage points without changing your spending habits. The CFPB’s credit utilization explainer confirms that the reported balance, not your end-of-month payoff, is what affects your score.

Request a Credit Limit Increase

If your spending stays constant but your limit rises, your utilization ratio drops automatically. For example, increasing a $5,000 limit to $10,000 while carrying a $2,000 balance drops utilization from 40% to 20%. Most major issuers — including Chase, Capital One, and American Express — allow limit increase requests online. Note that some requests trigger a hard inquiry, so ask whether a soft pull is available first.

Set up balance alerts with your credit card issuer so you are notified when your balance reaches a specific threshold — for example, 20% of your limit. This gives you time to make a mid-cycle payment before the statement closing date, keeping your reported utilization in the optimal range.

Avoid Closing Old Accounts

An old card with a zero balance contributes available credit to your total limit — reducing your utilization ratio passively. Closing it removes that buffer. Unless a card carries a high annual fee that outweighs the benefit, keeping older accounts open is generally the right call. This also supports the length-of-credit-history factor in your FICO score. For a broader look at managing your overall financial picture, exploring smart savings habits can free up cash to pay down balances faster.

What Common Mistakes Destroy Your Credit Utilization Ratio?

The most damaging mistakes are closing paid-off cards, making only minimum payments, and allowing a single card to creep toward its limit while ignoring it.

Minimum Payments and the Utilization Trap

Making only the minimum payment on a credit card barely reduces your balance. On a $5,000 balance with a 20% APR, the minimum payment might be as low as $100–$125 per month — leaving the utilization ratio virtually unchanged. Meanwhile, interest compounds. Understanding how compounding works against you in high-utilization situations makes the urgency of aggressive paydown clear.

Opening Multiple New Cards at Once

While opening a new card increases your total available credit, applying for several cards in a short window triggers multiple hard inquiries and signals financial stress to lenders. FICO counts multiple hard inquiries within a 45-day window as one for rate-shopping purposes for mortgages and auto loans — but that exception does not apply to credit cards. Space out applications by at least six months when possible.

If your credit profile has been damaged by high utilization or missed payments, rebuilding is possible with disciplined habits. The framework for rebuilding your finances from a low point applies directly to credit recovery strategies.

“The single biggest mistake people make is thinking that paying on time is enough. You can have a perfect payment history and still have a mediocre score if your balances are too high relative to your limits.”

Ignoring Your Credit Report

Errors on your credit report — such as a balance that was paid off but still shows as outstanding — can inflate your reported utilization artificially. Under the Fair Credit Reporting Act (FCRA), you are entitled to dispute inaccurate information with Equifax, Experian, and TransUnion directly. Checking your report at least once per year at AnnualCreditReport.com is a foundational habit. You can also monitor for potential discrimination in credit-related accounts — the CFPB’s work on auto loan bias illustrates how reporting errors and systemic issues can affect borrowers.

Frequently Asked Questions

How quickly does credit utilization affect your credit score?

Changes to your credit utilization ratio are reflected in your score within one billing cycle — typically 30 days. Once your issuer reports a lower balance to the credit bureaus, the score update follows within days. This makes utilization the fastest factor to improve short-term.

Does credit utilization ratio reset every month?

Yes. Utilization is not a running historical average — it reflects your current reported balances relative to current limits at the time of scoring. Paying down a balance this month can produce a score improvement by next month’s report date.

Is 30% credit utilization the hard cutoff?

The 30% threshold is a widely cited guideline, not a hard cutoff. Any reduction in utilization improves your score incrementally. Scoring models treat lower utilization more favorably at every step — 29% scores better than 31%, but 9% scores better than 29%. Aim as low as practically possible.

Does a high credit utilization ratio mean you will be denied credit?

High utilization does not automatically result in denial, but it lowers your score — which can push you into higher interest rate tiers or trigger denial at lenders with stricter cutoffs. Lenders also review utilization directly as part of manual underwriting, independent of your score.

Does paying off a credit card in full each month help utilization?

Paying in full helps you avoid interest, but it does not guarantee a low reported utilization. If your balance is high at the statement closing date, that balance gets reported — even if you pay it the next day. To show low utilization, pay down before the statement closes, not just before the due date.

Does a balance transfer affect my credit utilization ratio?

A balance transfer moves debt from one card to another but does not reduce your total revolving balance. Your overall utilization stays the same. However, per-card utilization shifts — which can help or hurt depending on the limits of the cards involved. It only improves your ratio if the destination card has a higher limit than the source card.

Do business credit cards affect personal credit utilization?

Most small-business credit cards from major issuers — including Chase Ink, American Express, and Capital One Spark — do not report to personal credit bureaus for routine activity. However, some do report, and nearly all will report delinquencies. Check your issuer’s reporting policy to know whether business card balances affect your personal credit utilization ratio.

Sources

- myFICO — What’s in Your Credit Score

- myFICO — Credit Utilization and Your Score

- Experian — What Is a Good Credit Utilization Rate?

- Experian — How Does Credit Utilization Affect Your Score?

- Consumer Financial Protection Bureau — Credit Reports and Scores

- CFPB — What Is a Credit Utilization Rate?

- VantageScore — Credit Score Basics for Consumers

- AnnualCreditReport.com — Free Official Credit Reports

- Equifax — Understanding Your Credit Utilization Rate

- National Foundation for Credit Counseling — Credit Resources