Key Takeaways

- The average American household wastes $5,400/year on brand-name premiums, unnecessary bank fees, and overpriced everyday items — switching to equivalent alternatives saves that amount with zero lifestyle downgrade.

- Store-brand groceries are 25–40% cheaper than name brands, and Consumer Reports testing shows identical quality in 73% of categories including cereal, canned goods, cleaning supplies, and OTC medications.

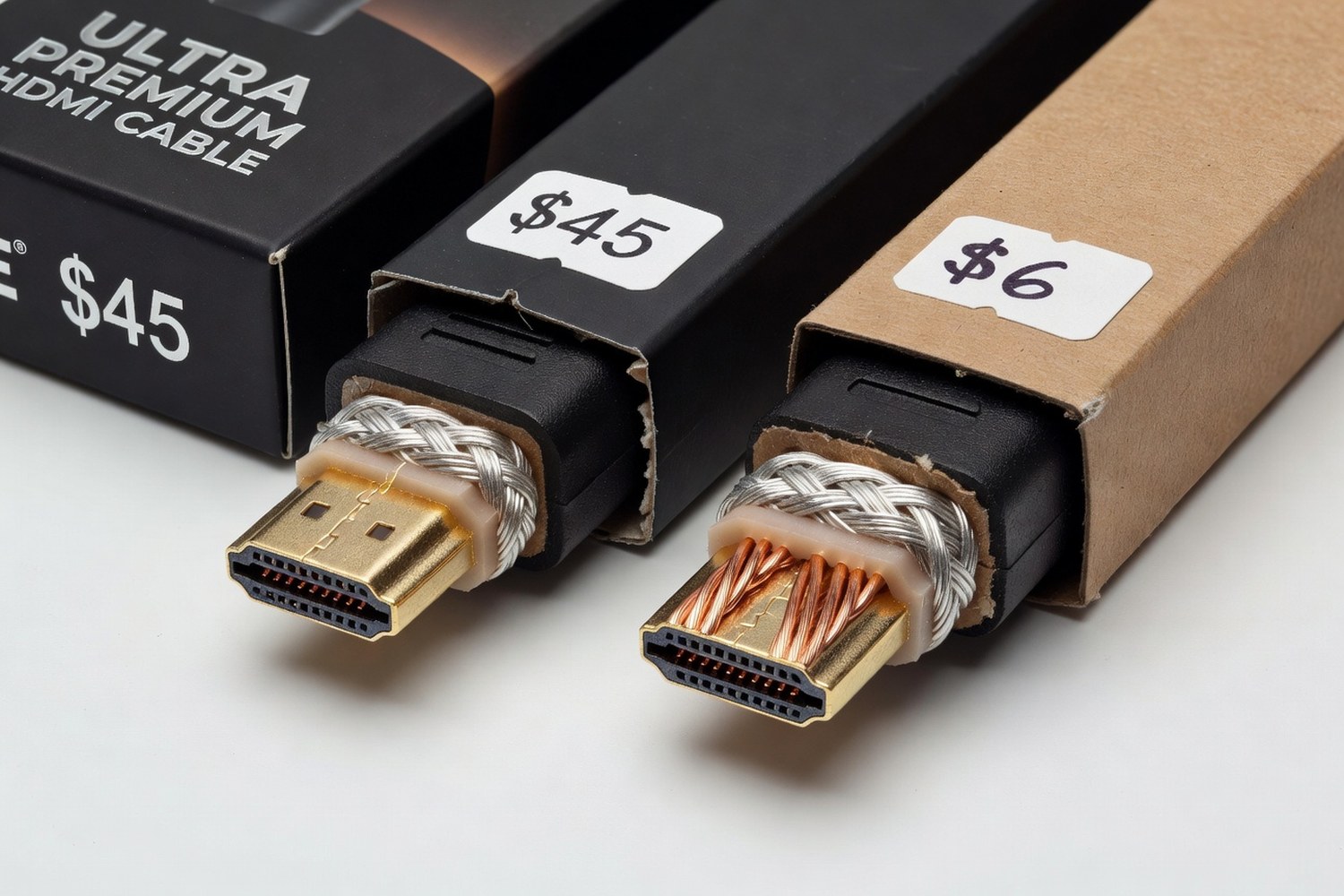

- Premium HDMI cables ($40–$80) transmit an identical digital signal to $6 cables — the “gold-plated” premium is pure marketing with zero measurable quality difference in independent testing.

- Switching from a traditional bank ($144/year in fees) to an online bank ($0/year) and from a gym membership ($600/year) to a bodyweight/outdoor routine saves $744/year before touching any other category.

Table of Contents

- The Brand-Name Premium: What You’re Really Paying For

- Groceries: Store Brands vs. Name Brands (The Data Is Clear)

- Electronics & Cables: The $6 Product That’s Identical to the $80 One

- Banking Fees: $144/Year You Don’t Have to Pay

- Personal Care: Razors, Skincare & The Markup Game

- Subscriptions You Forgot You’re Paying For

- Pets, Clothing & Other Surprisingly Overpriced Categories

- Frequently Asked Questions

The Brand-Name Premium: What You’re Really Paying For

When you buy Tide instead of the store-brand detergent sitting right next to it, you’re paying for one thing: the name. Not a better formula — the FTC doesn’t require brand-name products to be chemically different from generics. Not better ingredients — many store brands are manufactured in the same facilities as the brand-name version. You’re paying for advertising, shelf placement fees, and a logo. That premium adds up to roughly $5,400 per year for the average American household across all spending categories, according to Bureau of Labor Statistics consumer expenditure data.

I’m not saying every generic product is identical to every brand product. Some categories genuinely differ (coffee, certain cheeses, specific tools). But for the 8 categories I’m about to walk through, the evidence is overwhelming: you’re paying 25–400% more for a product that performs identically in blind tests. That’s not brand loyalty. That’s a marketing tax on your budget.

Here’s what $5,400/year in recovered overpayments buys you: a maxed-out Roth IRA ($7,000 contribution limit, almost covered), 18 months of aggressive credit card payoff, or the down payment on a used car in under 2 years. The money is there — it’s just hiding in line items you’ve never questioned. Paying your credit card early with these savings amplifies the benefit even further.

Groceries: Store Brands vs. Name Brands (The Data Is Clear)

Groceries are the single biggest overpayment category for most households. The average family of four spends $1,100/month on food, and switching 60% of brand-name purchases to store-brand equivalents saves $250–$350/month — that’s $3,000–$4,200/year.

Consumer Reports blind-tested 65 categories of store-brand versus name-brand groceries. The result: 73% of store brands were rated equal or better than their name-brand counterparts in taste, performance, and quality. The categories where store brands consistently matched: cereal, canned vegetables, frozen vegetables, cooking oil, butter, pasta, cleaning supplies, paper towels, and over-the-counter medications (which are FDA-required to contain identical active ingredients).

The categories where brand names sometimes win: coffee (subjective taste preference), cheese (artisan varieties), and chocolate. Everything else? You’re paying for packaging. Kirkland (Costco), Great Value (Walmart), 365 (Whole Foods), and Good & Gather (Target) are all manufactured by the same companies that make the brand-name versions. Same factory, same ingredients, different label — 30% lower price. The CFPB consumer tools section has additional resources for comparison shopping.

| Item Category | Brand-Name Price | Store-Brand Price | Quality Difference | Annual Savings (switching) |

|---|---|---|---|---|

| Cereal | $4.79/box | $2.99/box | None (blind test equal) | $94 |

| OTC Pain Relief | $9.99/100ct | $3.49/100ct | None (FDA identical) | $78 |

| Cleaning Supplies | $5.49/bottle | $2.79/bottle | Minimal | $130 |

| HDMI Cables | $40–$80 | $6–$10 | Zero (digital = digital) | $34–$70 per cable |

| Razors (per cartridge) | $4.50–$6.00 | $1.50–$2.50 (safety razor) | Comparable or better | $150–$250 |

Brand-name vs. store-brand/alternative pricing comparison. Sources: Consumer Reports, BLS, FTC. Verified March 2026.

⚡ Pro Tip

Over-the-counter medications are the single most overpaid category in America. The FDA requires store-brand ibuprofen, acetaminophen, and allergy meds to contain the exact same active ingredient in the exact same dosage as the brand-name version. Advil ibuprofen 200mg: $9.99/100ct. Costco Kirkland ibuprofen 200mg: $3.49/500ct. That’s 93% less per pill for a chemically identical product. Check the “Drug Facts” label — if the active ingredient and dosage match, the product is functionally identical.

Electronics & Cables: The $6 Product That’s Identical to the $80 One

HDMI cables are the poster child for premium pricing with zero premium quality. HDMI transmits a digital signal — it either arrives perfectly or it doesn’t. There is no “better quality” digital signal. A $6 Amazon Basics HDMI cable delivers bit-for-bit identical picture and sound to an $80 Monster cable. This has been proven in independent testing by Wirecutter, CNET, and multiple engineering labs. The gold-plated connectors? Marketing. Gold conducts marginally better than copper in analog systems — HDMI is digital. It’s irrelevant.

The same applies to USB cables (use the cheapest certified cable — $3–$8), printer ink (third-party cartridges at 60–80% less, with no proven quality difference for standard printing), and phone screen protectors ($3 tempered glass from Amazon provides identical protection to $40 brand-name versions in drop tests).

Where electronics premiums ARE worth paying: laptops (build quality matters for 5+ year lifespan), noise-canceling headphones (audio processing requires engineering investment), and power strips with surge protection (UL certification matters for safety). For passive accessories — cables, adapters, cases, screen protectors — buy the cheapest option that has decent reviews and save the difference.

Banking Fees: $144/Year You Don’t Have to Pay

The average traditional bank charges $12/month in maintenance fees, $35 per overdraft, and $2.50 per out-of-network ATM transaction. That’s $144/year in base fees before a single overdraft. The FDIC reports that the average checking account holder pays $8–$12/month in total fees — $96–$144/year for the privilege of storing your own money.

Online banks charge $0 for all of this. SoFi, Ally, Capital One 360, and Marcus by Goldman Sachs offer no-monthly-fee checking, no overdraft fees (or $0 overdraft protection), and ATM fee reimbursement up to $10–$15/month. Some even pay 0.5–1% APY on checking balances — meaning your money grows instead of shrinking. The switch takes 30 minutes, and most online banks handle the transfer of direct deposits and autopay for you.

Overdraft fees alone cost Americans $15.5 billion in 2023. The CFPB has actively pushed for overdraft reform, and many banks have reduced or eliminated these fees — but only if you ask or switch to an account type that excludes them. Don’t wait for your bank to voluntarily stop charging you. Switch to a bank that doesn’t charge in the first place.

Personal Care: Razors, Skincare & The Markup Game

The razor industry is a masterclass in manufactured spending. A 4-pack of Gillette Fusion cartridges costs $18–$24 — that’s $4.50–$6.00 per cartridge. A double-edge safety razor handle costs $25–$40 once, and replacement blades cost $0.08–$0.25 each. After the initial handle purchase, you save $150–$250/year shaving the same number of times with the same (or closer) results. The “5-blade technology” that justifies the premium? Marketing. Dermatologists consistently recommend fewer blades (1–2) for less irritation.

Skincare follows the same pattern. A $65 moisturizer from a prestige brand contains the same active ingredients (hyaluronic acid, niacinamide, retinol) as a $12 CeraVe or Neutrogena product. Dermatologists — the actual skin experts, not influencers — overwhelmingly recommend drugstore brands over luxury lines. The NIH’s dermatology research shows no clinical difference between $15 and $150 sunscreens when the SPF and active ingredients match.

Hair care: salon-exclusive shampoos ($25–$40/bottle) contain the same surfactants as drugstore versions ($5–$8). If your hairstylist says only salon products work, ask them to identify the active ingredient difference — most can’t, because there isn’t one in most cases.

⚡ Pro Tip

Before buying any skincare or personal care product, check the active ingredient list (not the marketing name) and search for it on EWG’s Skin Deep database or the NIH PubMed database. If a $65 serum’s key ingredient is “niacinamide 5%,” search for “niacinamide 5%” — you’ll find the same concentration in $12 products. The cosmetics industry spends $21 billion/year on advertising specifically to prevent you from making this comparison. Five minutes of ingredient research saves hundreds per year.

Subscriptions You Forgot You’re Paying For

The average American pays for 12 active subscriptions totaling $219/month, according to BLS consumer data. But here’s the staggering part: when surveyed, most people estimate they spend $86/month on subscriptions — underestimating by 155%. The gap is forgotten subscriptions, trials that auto-converted, and services you signed up for once and stopped using.

Audit your bank and credit card statements for the past 3 months. Flag every recurring charge. For each one, ask: “Did I use this in the past 30 days?” If no, cancel it. The average person finds $40–$80/month in unused subscriptions — that’s $480–$960/year recovered in 20 minutes of statement scanning.

The biggest offenders: gym memberships ($50–$80/month, with 67% of members not going regularly), streaming services (the average household pays for 4.7 streaming services but watches 2.3), premium app subscriptions (cloud storage, music, meditation apps that have free alternatives), and insurance products you didn’t realize you signed up for (identity theft monitoring, phone insurance, extended warranties that duplicate your credit card’s coverage).

Pets, Clothing & Other Surprisingly Overpriced Categories

A few more categories where the premium-to-value ratio is upside down:

Designer pets vs. shelter adoption. A purebred puppy from a breeder costs $1,500–$5,000. A shelter adoption costs $50–$400 and includes spay/neuter, vaccinations, and microchipping ($300–$600 value). The shelter dog is no less loving, loyal, or healthy — and you’ve saved a life while saving $1,100–$4,600. The SBA notes that pet spending is the fastest-growing consumer category, making cost awareness even more important.

New clothing vs. thrifted. A new pair of brand-name jeans costs $60–$150. The identical pair (sometimes with tags still on) at a thrift store costs $8–$20. ThredUp, Poshmark, and local Goodwill stores carry current-season clothing at 70–90% discounts. Buying 50% of your wardrobe secondhand saves the average person $800–$1,500/year.

Bottled water vs. filtered tap. A household buying bottled water spends $300–$600/year. A Brita or PUR filter costs $25–$40 and replacement filters run $6–$8 every 2 months. Annual cost of filtered tap: $62. The water quality is equivalent or better in most U.S. municipalities — the EPA regulates tap water more strictly than the FDA regulates bottled. Check your city’s EPA water quality report to verify.

Frequently Asked Questions

What everyday items do most people overpay for?

The biggest overpayment categories are brand-name groceries (25 to 40% premium over identical store brands), premium cables and electronics accessories (200 to 600% markup for identical digital performance), bank fees ($144 per year average at traditional banks versus $0 at online banks), razor cartridges ($4.50 to $6 per cartridge versus $0.08 to $0.25 for safety razor blades), and forgotten subscriptions ($40 to $80 per month average waste).

Are store-brand products really the same quality as name brands?

In 73% of categories tested by Consumer Reports, store brands rated equal or better than name brands in blind tests. Over-the-counter medications are FDA-required to contain identical active ingredients and dosages. Many store brands are manufactured in the same facilities as name brands. Categories where brands sometimes win: coffee, artisan cheese, and chocolate. Everything else is essentially the same product with a different label.

How much can I realistically save by switching to cheaper alternatives?

The average household can save $5,400 per year across all categories: $3,000 to $4,200 on generic groceries, $744 on banking fees and unused gym memberships, $480 to $960 on forgotten subscriptions, $150 to $250 on razors, and $200 to $500 on electronics accessories. These are conservative estimates requiring zero lifestyle sacrifice.

Are expensive HDMI cables actually better than cheap ones?

No. HDMI transmits a digital signal that either arrives perfectly or doesn’t. A $6 Amazon Basics cable delivers bit-for-bit identical picture and sound to an $80 premium cable. This has been confirmed by Wirecutter, CNET, and independent engineering labs. Gold-plated connectors provide zero benefit for digital signals. Save the $74 difference per cable.

Is it worth switching from a traditional bank to an online bank?

Yes. Traditional banks charge an average of $12 per month in maintenance fees plus $35 per overdraft. Online banks like Ally, SoFi, and Capital One 360 charge $0 for checking, $0 for overdraft, and reimburse ATM fees up to $10 to $15 per month. Some pay 0.5 to 1% APY on checking balances. The switch takes 30 minutes and saves $144 to $500 per year depending on your overdraft frequency.

References

- Bureau of Labor Statistics, 2026, “Consumer Expenditure Survey — Household Spending,” bls.gov

- Federal Trade Commission, 2026, “Consumer Protection — Product Marketing Standards,” ftc.gov

- Consumer Financial Protection Bureau, 2026, “Overdraft and Banking Fee Data,” consumerfinance.gov

- Federal Deposit Insurance Corporation, 2026, “Consumer Banking Fees Report,” fdic.gov

- National Institutes of Health, 2026, “Dermatology Research — Skincare Ingredient Efficacy,” nih.gov

- Environmental Protection Agency, 2026, “Drinking Water Quality Standards,” epa.gov

- Consumer Financial Protection Bureau, 2026, “Consumer Tools — Shopping Comparison,” consumerfinance.gov

- Federal Reserve Board, 2026, “Consumer Spending Patterns — Survey of Consumer Finances,” federalreserve.gov

- Small Business Administration, 2026, “Consumer Spending Trends by Category,” sba.gov

- Federal Trade Commission, 2026, “Advertising and Marketing Rules,” ftc.gov

Keep Reading

More on smart spending and saving money: