Key Takeaways

- Paying your credit card before the statement closing date (not just the due date) lowers the balance that gets reported to credit bureaus — dropping utilization from 45% to 10% can boost your FICO by 30–50 points within one billing cycle.

- The average American carries $6,580 in credit card debt at 22.8% APR. Paying the full balance 2 weeks early saves $1,499 in annual interest versus making minimum payments — and $125 more than paying on the due date due to daily interest accrual.

- Credit card interest accrues daily (not monthly), so a $5,000 balance at 22.8% APR generates $3.12 in interest every single day. Paying 14 days early saves roughly $43.70 per billing cycle — $524 per year.

- Paying early before the statement closes creates a “reporting advantage” — your card shows a lower balance on your credit report even if you charge the same amount monthly, which directly improves your creditworthiness for mortgages and auto loans.

Table of Contents

- How Daily Interest Accrual Makes Early Payments Worth More

- Statement Closing Date vs. Due Date: Why the Difference Matters

- The Credit Score Impact of Paying Before Statement Close

- Exactly How Much You Save by Paying Early

- The Multiple Payment Strategy: Pay Twice a Month

- Setting Up Autopay That Actually Works

- When Paying Early Doesn’t Help (and What to Do Instead)

- Frequently Asked Questions

How Daily Interest Accrual Makes Early Payments Worth More

Most people think credit card interest is calculated monthly. It’s not. Interest accrues daily — and that daily compounding is exactly why paying early saves you real money, even compared to paying on time.

Here’s the math: the average credit card APR is 22.8%. Your daily periodic rate is 22.8% ÷ 365 = 0.0625% per day. On a $5,000 balance, that’s $3.12 in interest accruing every single day. Pay 14 days before your due date instead of on it, and you avoid $43.68 in interest that billing cycle. Over 12 months? $524.16. That’s money you keep just by moving the payment earlier in the month. No extra payments needed. Same amount of money, different timing.

The Consumer Financial Protection Bureau notes that the average American household carries $6,580 in revolving credit card debt. At 22.8% APR with minimum payments, that balance takes 17 years to pay off and costs $8,943 in interest. But even households paying in full every month benefit from early timing — because the statement balance affects your credit score, and your credit score affects every other interest rate in your life.

I want to make something clear: the best strategy is paying your full balance every month. But when you pay within that month matters more than most people realize. Let me break down exactly why — and the specific dates to target. If you’re carrying a balance and want to understand how it affects your car loan or mortgage rate, our credit score guide connects the dots.

Statement Closing Date vs. Due Date: Why the Difference Matters

Your credit card has two critical dates, and confusing them costs money:

Statement closing date: The day your billing cycle ends and your issuer calculates your balance. This is the number reported to credit bureaus. Typically falls 21–25 days before your payment due date.

Payment due date: The last day to pay without incurring a late fee. Usually 21–25 days after the statement closes.

Here’s the insight most people miss: credit bureaus see your balance as of the statement closing date, not your payment date. If you charge $3,000 during the month and pay it in full on the due date, your credit report shows $3,000 in utilization for that entire billing period. But if you pay $2,500 before the statement closes and only $500 remains when the statement cuts, the bureaus see $500. Same spending. Same total payment. Dramatically different credit score impact.

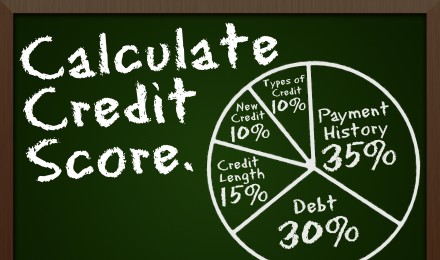

On a card with a $5,000 limit, the difference is 60% reported utilization versus 10%. FICO treats utilization as the second most important factor (30% of your score). Dropping from 60% to 10% can boost your score by 40–60 points. That matters enormously if you’re about to apply for a mortgage — the difference between 6.5% and 7.5% on a $300,000 mortgage is $72,000 in total interest over 30 years. A credit card’s reported balance doesn’t just affect that card — it affects every rate you’re offered everywhere.

| Payment Timing | Balance Reported to Bureaus | Utilization ($5K limit) | FICO Impact | Interest Saved vs. Minimum |

|---|---|---|---|---|

| Pay before statement close | $0–$500 | 0–10% | +40 to +60 points | $1,499+/year |

| Pay in full on due date | $3,000 (full cycle spend) | 60% | Neutral | $1,374/year (no interest) |

| Pay minimum on due date | $3,000+ | 60%+ | -20 to -40 points | $0 (paying $1,499/yr in interest) |

| Miss payment | $3,000+ (plus late fee) | 60%+ rising | -60 to -110 points | Negative (adding $35+ late fees) |

Credit card payment timing comparison on $3,000 monthly spend / $5,000 limit. Rates as of March 2026.

The Credit Score Impact of Paying Before Statement Close

Let me make this concrete with a real scenario. You use your credit card for $2,500 in monthly expenses. Your credit limit is $5,000. If you pay $2,500 on the due date, your statement showed $2,500 — that’s 50% utilization. Your FICO treats that as moderate risk.

Same spending, different timing: you make a $2,000 payment 3 days before your statement closes. The statement shows $500. That’s 10% utilization — well within the optimal range. Your FICO could be 40–60 points higher, even though you spent and paid the exact same amount.

Why does this matter so much? Because utilization is 30% of your FICO score and it has zero memory. Unlike payment history (which tracks 7 years), utilization only measures the current snapshot. You can go from 80% utilization to 10% in a single billing cycle and get the full score benefit immediately. That’s why this strategy is the fastest legal credit score boost available — and it’s completely free. Our bad credit car loan guide uses this exact technique as step one.

⚡ Pro Tip

Find your exact statement closing date by logging into your card’s online portal or calling the number on the back. Set a calendar reminder for 3 days before that date. Make your payment then — before the statement cuts. Your utilization will report at the post-payment level, not the peak-spending level. For maximum impact, pay down to under 10% of your limit before the closing date. On a $10,000 limit card, keeping the reported balance under $1,000 puts you in the optimal FICO utilization tier — worth 20–50 points versus a 30–50% utilization report.

Exactly How Much You Save by Paying Early

Let’s run real numbers on three scenarios — all on a $5,000 balance at 22.8% APR:

Scenario 1: Minimum payment only ($125/month). Payoff time: 5.3 years. Total interest paid: $2,902. Total cost: $7,902 on $5,000 in purchases. You paid 58% more than you bought.

Scenario 2: Full balance on due date. Payoff time: immediate. Total interest paid: $0 (if you’re within the grace period and paid last month’s balance in full). This is the target everyone should aim for.

Scenario 3: Full balance 14 days before due date. Same as scenario 2 for interest savings — but with the added benefit of lower reported utilization, boosting your credit score and qualifying you for better rates on everything else. If you carry a partial balance, the 14-day early payment saves $524/year in daily interest accrual compared to paying on the due date.

The takeaway: pay in full (non-negotiable for financial health), and pay early (bonus optimization for credit score and residual interest savings). The Federal Reserve’s G.19 consumer credit data shows the average household pays $1,380/year in credit card interest — nearly all of which is avoidable.

The Multiple Payment Strategy: Pay Twice a Month

Here’s my favorite technique for people who want to optimize without overthinking: make two payments per month instead of one. Split your expected monthly bill in half and pay every two weeks.

If you normally spend $2,000/month on your card, pay $1,000 on the 1st and $1,000 on the 15th. Benefits: your average daily balance drops by roughly 50% (cutting daily interest accrual in half if you carry a balance), your reported utilization stays low because the balance never peaks as high, and you make 26 half-payments per year instead of 12 full payments — the equivalent of 13 monthly payments.

For balance carriers, the biweekly approach on $5,000 at 22.8% APR saves about $680/year in interest compared to one monthly payment — just from reducing the average daily balance. Combined with the credit score benefit of lower reported utilization, it’s a double win. The same biweekly principle works on student loans and mortgages too.

| Payment Strategy | Annual Interest ($5K at 22.8%) | Reported Utilization | FICO Benefit |

|---|---|---|---|

| Minimum once/month | $1,140 | 80–100% | Negative |

| Full once/month on due date | $0 | 40–60% | Neutral |

| Full before statement close | $0 | 0–10% | +40 to +60 points |

| Biweekly (2x/month) | $0 (or $460 if carrying balance) | 10–25% | Strong positive |

Credit card payment frequency comparison. Source: CFPB, Federal Reserve. Verified March 2026.

Setting Up Autopay That Actually Works

Autopay is the safety net that ensures you never miss a payment — but most people set it up wrong. Here’s the right way:

Set autopay to “full statement balance” — not “minimum payment.” Minimum-payment autopay is a trap that costs you thousands in interest while giving you false peace of mind. Full-balance autopay eliminates interest charges entirely. If you’re worried about a large unexpected charge, keep a cash buffer equal to 1.5x your average monthly card spend in your checking account.

Set it 5 days before the due date, not on the due date. Processing delays happen. Weekends and bank holidays push transactions to the next business day. A payment initiated on Friday may not post until Monday or Tuesday. By scheduling 5 days early, you build in a buffer that prevents late payments — which cost $35 in fees plus 60–110 FICO points for a 30-day delinquency. The CFPB confirms that even one 30-day late payment stays on your credit report for 7 years.

Pair autopay with a manual pre-statement payment. Set autopay as your safety net (catches anything you miss), but also make a manual payment 3 days before your statement closing date to control your reported utilization. This two-layer approach gives you both interest savings and credit score optimization. Most card issuers let you enable autopay and still accept manual payments in the same billing cycle.

⚡ Pro Tip

Most credit card issuers offer an automatic 0.25% rate reduction for enrolling in autopay — and if they don’t advertise it, calling and asking often unlocks it. On a $5,000 average balance, 0.25% saves $12.50/year — small, but free money. More importantly, autopay enrollment signals responsible borrowing to lenders. Some credit card companies use autopay status as an internal factor when considering credit limit increases. A higher limit with the same spending automatically lowers your utilization ratio, creating a virtuous cycle.

When Paying Early Doesn’t Help (and What to Do Instead)

Early payment isn’t a magic fix for every situation. Here’s when it doesn’t move the needle — and what actually helps:

If you’re only making minimum payments. Paying the minimum a week early versus on the due date saves about $5/month in daily interest. That’s nice but meaningless when you’re paying $95/month in interest on a $5,000 balance. The real fix is paying more than the minimum — even $50 extra makes a bigger difference than any timing optimization. Focus on amount first, timing second.

If you have 0% intro APR. During a promotional rate period, no interest accrues regardless of when you pay. Timing is irrelevant for interest savings. But paying before the statement close still matters for utilization reporting — so if you’re applying for a mortgage or car loan during your promo period, the timing trick still helps your credit score.

If you’re trying to fix severely damaged credit. Early payment optimizes an already-functional credit profile. If you have late payments, collections, or charge-offs, those issues dwarf any utilization benefit. Fix the fundamentals first: bring all accounts current, dispute errors on your report, and then use early-payment timing to polish your score. Our bad credit recovery guide covers the step-by-step repair process.

Frequently Asked Questions

Does paying my credit card early actually save money on interest?

Yes if you carry a balance. Credit card interest accrues daily at your APR divided by 365. On a $5,000 balance at 22.8%, that’s $3.12 per day. Paying 14 days early saves $43.68 per billing cycle or $524 per year. If you pay in full each month and have a grace period, the interest savings are minimal but the credit score benefit remains significant.

When exactly should I pay my credit card for the best credit score?

Pay 3 to 5 days before your statement closing date (not the due date). This ensures the balance reported to credit bureaus reflects your post-payment amount. Keeping reported utilization under 10% of your credit limit maximizes your FICO score. Find your statement closing date in your card’s online portal or on your most recent statement.

Is it bad to pay your credit card bill too early?

No. There is no penalty or downside to paying early. Some people worry that paying before the statement generates means “no activity” is reported, but this is a myth. As long as you use the card during the billing cycle, activity is recorded. Paying early simply means a lower balance is reported, which improves your utilization ratio and credit score.

Should I pay my credit card in full or make multiple payments?

Both. Make one payment before the statement closes to reduce reported utilization, then let autopay handle the remaining balance on the due date. If you carry a balance, making two payments per month (biweekly) reduces your average daily balance by roughly 50%, saving $460 to $680 per year in interest on a $5,000 balance at 22.8% APR.

Does paying off my credit card raise my credit score immediately?

Utilization changes appear on your credit report within 1 to 2 billing cycles after the statement closing date. If you pay down a $4,000 balance to $500 before the statement closes, your report will show the lower balance within 30 days. The FICO score boost from reduced utilization is immediate once the updated balance is reported — there is no waiting period.

References

- Consumer Financial Protection Bureau, 2026, “Credit Card Interest and Fees Explained,” consumerfinance.gov

- Federal Reserve Board, 2026, “Consumer Credit G.19 — Revolving Credit Data,” federalreserve.gov

- Consumer Financial Protection Bureau, 2026, “Credit Inquiries and Score Impact,” consumerfinance.gov

- Federal Trade Commission, 2026, “Credit Card Rights and Protections,” ftc.gov

- Federal Reserve Bank of New York, 2026, “Household Debt — Credit Card Balances,” newyorkfed.org

- Consumer Financial Protection Bureau, 2026, “Autopay and Payment Processing Rules,” consumerfinance.gov

- Federal Deposit Insurance Corporation, 2026, “Consumer Credit Card Practices,” fdic.gov

- Experian, 2026, “Credit Utilization and FICO Score Impact,” experian.com

- Federal Reserve Board, 2026, “Survey of Consumer Finances — Revolving Debt,” federalreserve.gov

- Consumer Financial Protection Bureau, 2026, “Submit a Complaint — Credit Cards,” consumerfinance.gov

Keep Reading

More on credit card strategy and credit building: