Key Takeaways

- The FAFSA is the single most important financial aid document you’ll ever fill out — it unlocks federal grants, loans, work-study, and most institutional aid, and it’s free to submit.

- File the FAFSA as early as possible after October 1 each year — many state and institutional grants are awarded on a first-come, first-served basis and run out.

- Your financial aid award letter will mix grants (free money), loans (money you repay), and work-study — read it carefully and don’t assume all “aid” is actually free.

- If your financial situation has changed significantly since last year’s taxes, you can appeal your aid offer — colleges have more flexibility than most families realize.

Table of Contents

What the FAFSA Actually Is

Let me tell you what no one explains clearly: the FAFSA isn’t just a form for poor families. It’s the key that unlocks almost every type of federal financial aid — including unsubsidized loans that virtually any student can receive regardless of income. If you skip the FAFSA, you’re locking yourself out of subsidized loans, Pell Grants, federal work-study, and most state grant programs. There is no scenario where skipping it makes financial sense.

FAFSA stands for Free Application for Federal Student Aid. It collects information about your family’s finances — income, assets, household size — and uses a formula to determine your Student Aid Index (SAI), which colleges use to calculate how much aid to offer you. It opens on October 1 each year for the following academic year. It’s free to submit. According to Federal Student Aid, millions of eligible students leave free grant money on the table every year simply by not filing.

⚡ Pro Tip

File the FAFSA on October 1 — the first day it opens for the following academic year. Many states and colleges award grants on a first-come, first-served basis until the money runs out. Filing in January instead of October can cost you thousands in grants you would have received. Set a calendar reminder right now.

Types of Financial Aid: Grants, Loans, Work-Study

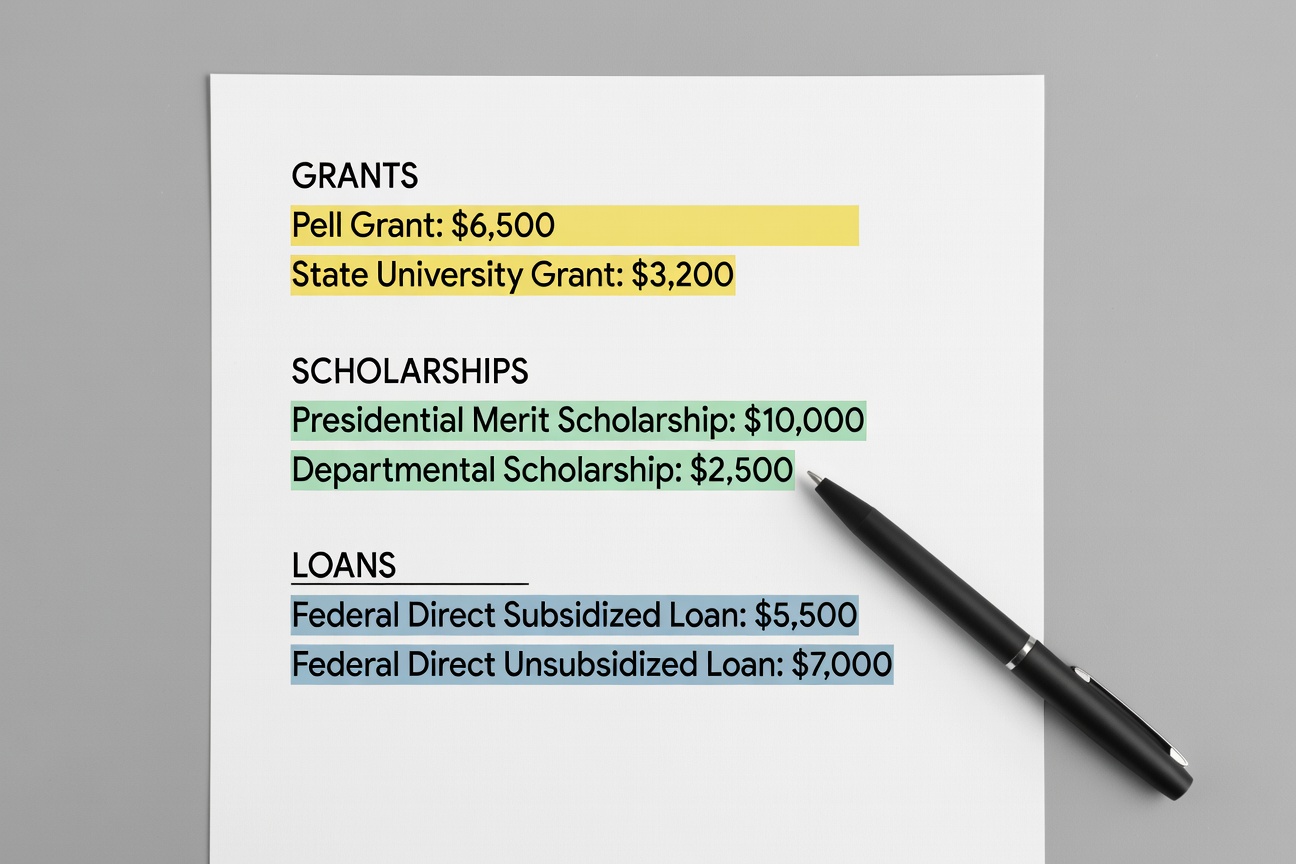

Not all financial aid is created equal — and the biggest mistake students make is treating everything in their award letter as “free money.” Here’s the breakdown you need:

Grants are actual free money. You don’t repay them. The Pell Grant is the largest federal grant program, worth up to $7,395 for the 2025–26 academic year for qualifying students. Many states have their own grant programs on top of this. Colleges also award institutional grants — these are the school’s own money, and they vary enormously based on your financial need and sometimes merit.

Work-Study is a federal program that subsidizes part-time jobs, usually on campus. It appears in your award letter as a dollar amount, but you earn it by working — it’s not deposited into your account. The jobs are flexible around class schedules and the earnings are paid directly to you as wages.

Loans are money you borrow and must repay with interest. They appear in your award letter right alongside grants, which confuses a lot of families. A school offering $30,000 in “financial aid” that turns out to be $5,000 grant + $25,000 loan isn’t being generous — it’s mostly debt. Read carefully.

| Aid Type | Source | Repay? | Key Facts |

|---|---|---|---|

| Pell Grant | Federal | No | Up to $7,395 (2025–26), need-based |

| Institutional Grant | College | No | Varies widely — merit and/or need |

| Federal Work-Study | Federal | No (earned) | Part-time campus job, paid as wages |

| Direct Subsidized Loan | Federal | Yes | Gov’t pays interest while in school |

| Direct Unsubsidized Loan | Federal | Yes | Interest accrues from disbursement |

| Rule of Thumb: Accept grants and work-study first. Accept subsidized loans before unsubsidized. Never take private loans until federal options are exhausted. | |||

The Financial Aid Timeline

The financial aid process runs on a strict annual cycle. October 1: FAFSA opens — file immediately, especially if you’re applying to schools with rolling aid or in states with first-come, first-served grants. December through February: most schools’ priority filing deadlines for maximum institutional aid consideration. February through April: award letters arrive as college acceptances come in. May 1: National Decision Day — most schools require your enrollment decision by this date. June onward: if you’re returning for another year, recertify your FAFSA and check if your SAI has changed.

Missing the October filing window doesn’t disqualify you from aid, but it can cost you state grants that have limited funding. Some of the most generous state programs — Cal Grant in California, TAP in New York — have specific filing deadlines that are non-negotiable.

Reading Your Award Letter

Your financial aid award letter is one of the most consequential documents you’ll receive, and colleges deliberately make them confusing. Some schools bundle loans and grants together under a single “aid” total. Others list work-study as if it’s already in your bank account. Here’s how to decode it:

First, separate all grants and scholarships (free money) from loans (debt) and work-study (earned wages). Add up only the grants and scholarships — that’s your actual gift aid. Subtract that from the total cost of attendance (tuition + fees + room + board + books + personal expenses). What remains is what you’ll need to cover through loans, work, savings, or family contribution. That number is the honest cost of attending that school. Do this for every school you’re considering before making a decision.

EFC vs. SAI: Understanding the Number That Drives Aid

For decades, the financial aid formula produced an Expected Family Contribution (EFC) — the amount the government determined your family could pay toward college. The FAFSA Simplification Act replaced EFC with the Student Aid Index (SAI) starting in the 2024–25 award year. The mechanics are similar but the formula changed significantly, affecting aid eligibility for millions of families.

Your SAI is calculated based on your family’s income, assets, family size, and number of college students in the household. A lower SAI means more financial need and potentially more grant aid. A SAI of zero means maximum Pell Grant eligibility. A SAI above a certain threshold means no Pell Grant eligibility — but you still qualify for federal loans regardless. The Federal Student Aid estimator can give you a rough SAI before you file.

How to Appeal Your Financial Aid Offer

This is the part most families don’t know they can do. If your financial situation has changed significantly since the tax year used on your FAFSA — job loss, divorce, unusual medical expenses, death of a parent — you can submit a professional judgment appeal to the financial aid office. Bring documentation. Be specific about what changed and by how much. Many schools have formal processes for this and genuine flexibility in their awards.

You can also appeal based on competing offers. If School A offered you $15,000 in grants and School B (your first choice) only offered $8,000, bring School A’s award letter to School B and ask them to match or improve it. This works more often than you’d expect, especially at private schools with large endowments. For more context on student loan options that may supplement your aid package, our comparison of federal vs. private student loans is essential reading.

⚡ Pro Tip

Never accept a financial aid offer without asking whether it can be improved. If you received a better offer from a comparable school, bring it to your preferred school’s financial aid office in writing and ask them to match it. Many schools have formal “professional judgment” processes for exactly this. The worst they can say is no — and a 10-minute conversation can be worth thousands of dollars.

The CSS Profile: When You’ll Need It

About 400 colleges — primarily private universities and some public flagships — require the CSS Profile in addition to the FAFSA. The College Board administers it, and unlike the FAFSA, it costs money to submit (though fee waivers are available). The CSS Profile goes deeper than the FAFSA — it asks about home equity, business assets, non-custodial parent finances, and more. Schools use it to award their own institutional aid, which at many private schools dwarfs the federal aid on offer.

If you’re applying to any of the 400+ CSS Profile schools, file it the same day you file the FAFSA. The priority deadlines often align. A full list of participating schools is available at cssprofile.collegeboard.org.

Putting It All Together

The financial aid process is genuinely manageable once you understand the structure. File the FAFSA on October 1. Submit the CSS Profile the same day if any of your schools require it. When award letters arrive, decode them properly — separate free money from debt. Compare the real net cost across schools. Appeal if your circumstances warrant it or if you have a competing offer. And before you accept any loans, read our breakdown of income-driven repayment options so you understand exactly what you’re signing up for.

For the savings side of the college funding equation, our guide to 529 plans in 2026 covers everything parents need to know about tax-advantaged college savings.

References

- Federal Student Aid (2026). “Filling Out the FAFSA.” studentaid.gov

- Federal Student Aid (2026). “How Much Aid Can I Get?” studentaid.gov

- Consumer Financial Protection Bureau (2025). “Paying for College.” consumerfinance.gov

- Investopedia (2025). “Financial Aid.” investopedia.com